The Premium That Didn't Drop When the Lien Did

You made the final payment on your 2015 Camry three months ago. The lender released the lien, you received the title, and your insurance premium stayed exactly where it was. You expected some change because the car is yours now and you drive it twice a week for groceries and medical appointments. The carrier kept charging the same amount for full coverage you're no longer required to carry.

This is the coverage-fit moment most retirees face but few insurance sites address directly. A paid-off vehicle driven lightly changes the replacement decision. Collision and comprehensive made sense when a lender required them and you commuted daily. Now you're deciding whether those premiums protect an asset worth self-insuring or whether liability alone leaves retirement savings exposed in an at-fault accident.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteArizona Bodily Injury Minimum Per Person

$25,000

Arizona requires $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage. These minimums protect the other driver, not your vehicle. A paid-off car means no lender requires collision or comprehensive, but liability limits protect your retirement assets if you cause an accident.

Arizona Revised Statutes § 28-4009

What Full Coverage Actually Protects Now

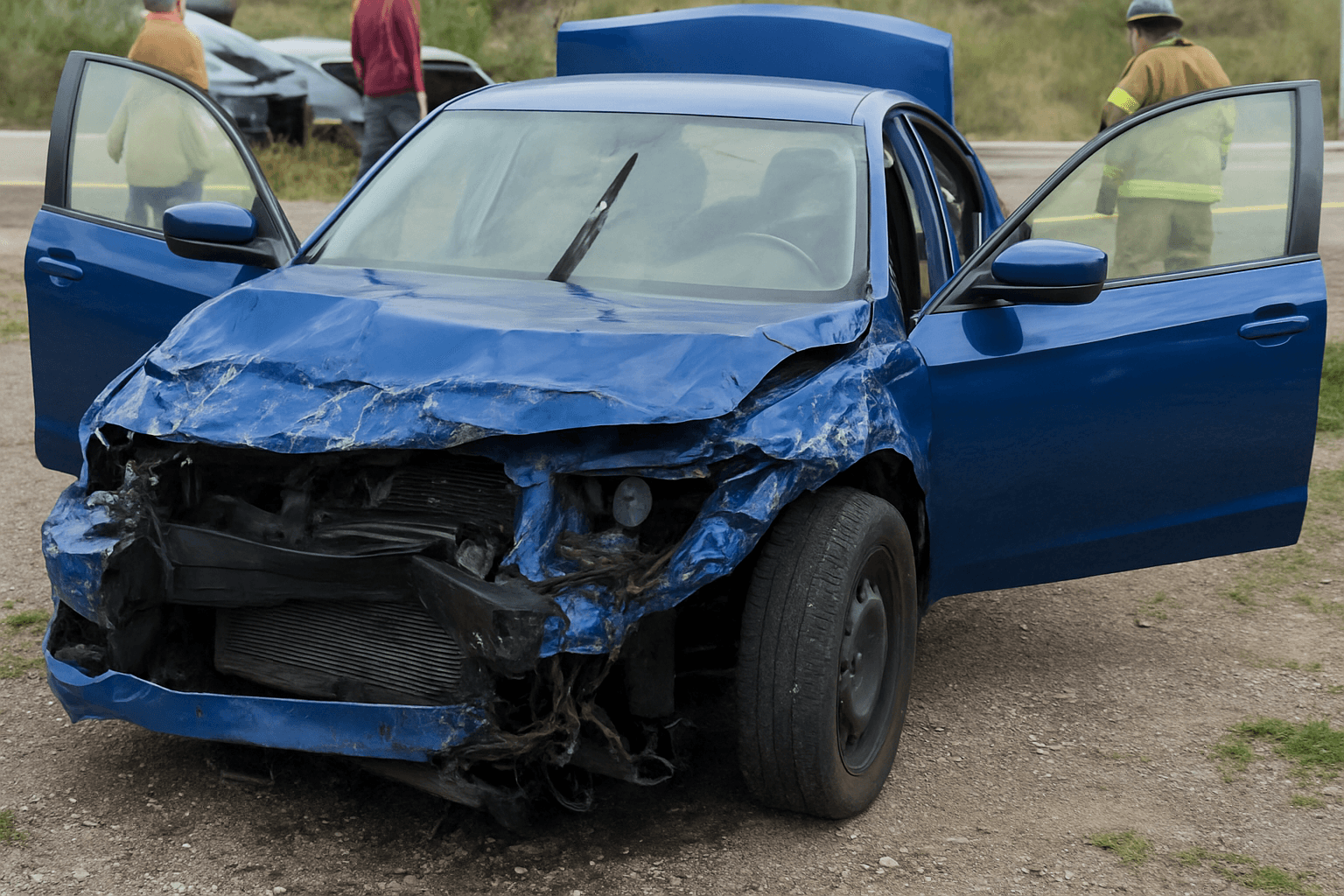

Liability insurance pays the other party when you cause an accident: their medical bills, their vehicle damage, their lost wages. It does not repair your car. That protection comes from collision coverage, which pays to fix or replace your vehicle after an accident regardless of fault, minus your deductible. Comprehensive coverage handles non-collision damage: theft, hail, fire, vandalism, hitting a deer.

When you financed the Camry, the lender required collision and comprehensive because their interest in the vehicle lasted until you paid the loan in full. Once you own it outright, that requirement vanishes. The decision shifts from what the lender mandates to what your household can absorb. If your car were totaled tomorrow, would you replace it from savings, or does the loss exceed what you can cover without financial strain?

The math is not about the premium alone. It is about replacement cost versus what the coverage costs annually. A 2015 Camry in good condition with 78,000 miles has a private-party value between $12,000 and $15,000 in the Scottsdale market. Collision and comprehensive combined typically represent a significant portion of your total premium. The question is whether that annual cost, compounded over the years you expect to drive the car, justifies the payout you would receive after the deductible if the vehicle were totaled.

The blocker: you lack the specific annual cost of your collision and comprehensive combined, and you do not know your car's current market value minus your deductible.

How to Run the Replacement Math

Request a declarations page from your carrier showing the premium breakdown by coverage type. Most carriers show liability, collision, comprehensive, and any optional coverages as separate line items. Add your collision and comprehensive annual costs together. Then check your vehicle's private-party value using Kelley Blue Book or Edmunds, entering your exact mileage, condition, and trim level. Subtract your deductible from that value. That net figure is what you would receive if the car were totaled tomorrow.

Compare the net payout to the annual premium cost. If your collision and comprehensive cost $600 annually and your car's value minus a $500 deductible is $11,500, you are paying roughly 5% of the net payout each year for that protection. Over three years you will have paid $1,800 in premiums for a vehicle whose value is declining. Many retirees conclude that beyond a certain depreciation point, self-insuring makes more financial sense than continuing coverage on an aging asset.

Related Articles

Liability Limits and Retirement Asset Exposure

Dropping collision and comprehensive does not reduce your liability exposure. In fact, it increases the importance of carrying liability limits well above Arizona's statutory minimums. If you cause an accident that injures another driver seriously, the $25,000 per-person bodily injury minimum will exhaust quickly. Medical bills from even a moderate injury can exceed that figure before the patient leaves the emergency room.

You are judgment-proof only if you have no assets to attach. Retirement accounts, home equity, and savings are all at risk in a lawsuit following an at-fault accident where your liability coverage proves insufficient. Many retirees carry $100,000 per person and $300,000 per accident in bodily injury liability, along with higher property damage limits, specifically because those limits protect what they spent decades accumulating.

The premium difference between state minimums and $100,000/$300,000 liability is modest compared to the asset exposure. When you drop collision and comprehensive, redirect a portion of that savings toward higher liability limits. The car is a depreciating asset you can replace from savings. Your retirement accounts and home equity are not.

Carriers Writing Auto Policies in Arizona

25

At least 25 carriers write personal auto policies in Arizona, with varying approaches to mature-driver and low-mileage programs. When adjusting coverage, compare how each carrier prices liability-only versus full coverage for a lightly driven paid-off vehicle. Some carriers price liability coverage more favorably for retirees than others.

Carrier license data verified via Arizona Department of Insurance

Low-Mileage Programs and Usage-Based Discounts

Most retirees in Scottsdale drive far less than they did during their working years. If you are logging under 7,500 miles annually, ask your carrier whether a low-mileage or usage-based program applies. Some carriers offer telematics programs that monitor mileage, braking, and speed; others offer a flat low-mileage discount based on your annual odometer reading submitted at renewal.

These programs can reduce your premium whether you carry full coverage or liability only. The savings apply to the entire policy, not just collision and comprehensive. If you decide to keep collision coverage on your paid-off car because the replacement math still works, a low-mileage discount reduces the annual cost you are weighing against the vehicle's value.

What Happens at the Next Accident or Total Loss

If you drop collision and comprehensive and then total your car in an at-fault accident, your carrier pays nothing toward your vehicle. You replace it from savings or you go without a car. If the other driver is at fault and carries adequate property damage liability, their carrier pays for your loss. If they are uninsured or underinsured, your uninsured motorist property damage coverage may apply, but only if you elected it and only up to the limit you chose.

This is not a scare tactic. It is the procedural reality. Retirees who self-insure their vehicle do so because they have determined the annual premium cost exceeds the financial risk of replacing the car from savings. That determination makes sense for many households with paid-off vehicles of moderate value driven lightly. It makes less sense for a household that cannot absorb a sudden $12,000 replacement expense without disrupting other financial plans.

Compare your emergency fund, your vehicle's current value, and your annual collision and comprehensive cost. If the coverage costs less than 10% of the vehicle's net value annually and you do not have liquid savings equal to replacement cost, keeping the coverage may still be the better path. If you have twice the vehicle's value in accessible savings and the coverage costs more than 10% of net value annually, dropping it and self-insuring becomes the financially rational choice.