When the Last Car Payment Changes Nothing

You made the final payment on your 2016 Camry three months ago. The renewal notice arrived last week with the same premium: full coverage, collision deductible unchanged, comprehensive still attached. The lender no longer requires it, but your carrier never mentioned dropping it. Most retirees in Chandler keep paying for collision coverage years after the loan ends because no one at renewal time asks whether it still earns its cost.

The decision is not whether collision is valuable in theory. The decision is whether the annual premium justifies itself against the vehicle's current market value, your annual mileage now that the commute is gone, and what you would actually receive after the deductible if you filed a total-loss claim tomorrow. That is arithmetic, not insurance advice. The carrier will keep billing for collision until you tell them to stop.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteArizona Bodily Injury Minimum Per Person

$25,000

Arizona requires $25,000 per person, $50,000 per accident bodily injury liability, and $15,000 property damage. Dropping collision and comprehensive leaves liability intact, which is the coverage protecting retirement assets in an at-fault accident.

A.R.S. Title 28, Financial Responsibility statutes

What Full Coverage Actually Protects

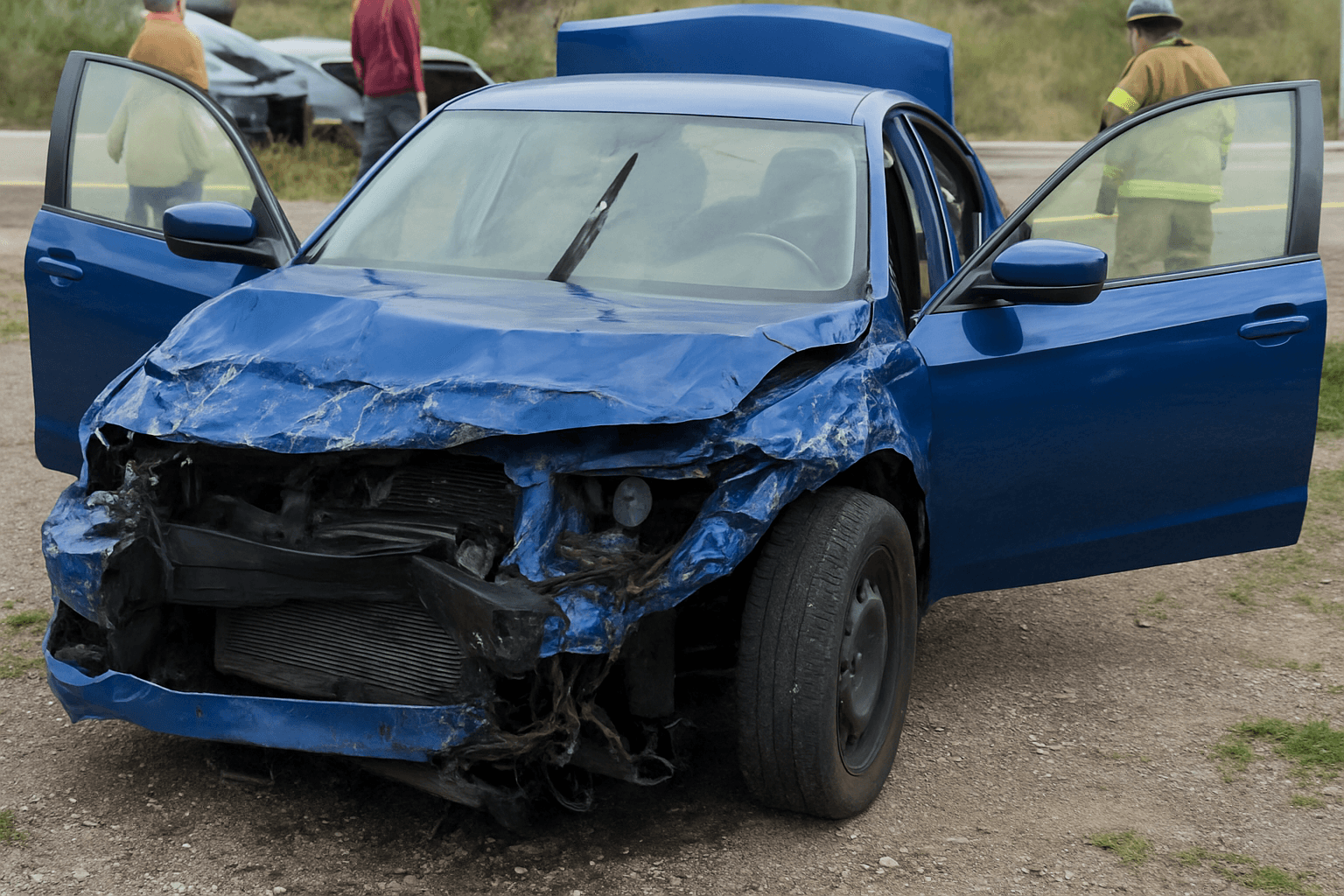

Full coverage means liability plus collision plus comprehensive. Liability pays the other driver's bills when you cause the accident. Collision pays to repair your car when you hit something or roll it. Comprehensive pays for theft, hail, vandalism, and animal strikes. The lender required collision and comprehensive because the car secured the loan. Once the title is yours, the only party protected by those coverages is you.

The question is whether the annual cost of protecting your car justifies the maximum payout you would receive. If your 2016 sedan is worth $8,500 and you carry a $1,000 deductible, a total loss pays $7,500. If collision and comprehensive together cost $650 per year, you recover the premium only if you total the car within roughly eleven years. Most retirees replace vehicles long before that window closes.

The blocker: you lack the current market value of your vehicle and the isolated annual cost of collision and comprehensive on your policy, so the payoff calculation remains unresolved.

How to Run the Coverage Math

Check your vehicle's current value using Kelley Blue Book or NADA Guides for private-party sale in good condition. Dealers and aggregators show trade-in values, which understate what you would receive in a total-loss settlement. Use the private-party figure. Subtract your deductible from that value to get your maximum net payout. If your sedan shows $8,200 private-party value and you carry a $1,000 deductible, your net payout ceiling is $7,200.

Call your agent or log into your carrier portal and request a quote for liability-only coverage: same limits, same deductibles removed, collision and comprehensive deleted. The difference between your current annual premium and the liability-only quote is what you pay per year to insure the vehicle itself. Divide your net payout ceiling by that annual cost. If the result is under three years, collision and comprehensive cost more than the car's value over a short holding period. That is when most Chandler retirees drop them.

Related Articles

State-Specific Quirks Arizona Retirees Face

Arizona does not mandate medical payments coverage or personal injury protection. If you drop collision and comprehensive but keep medical payments, verify whether Medicare coordinates as primary payer. Medicare Part B covers accident-related injuries regardless of fault, so med-pay on your auto policy may duplicate coverage you already carry. Most retirees in Chandler drop med-pay when they confirm Medicare applies, but coordination rules depend on whether you are still working or fully retired.

Arizona uses a fault-based system, so the at-fault driver's liability coverage pays your vehicle damage when they cause the accident. Uninsured motorist property damage is optional in Arizona, but it pays your repair costs when the at-fault driver carries no insurance or flees the scene. If you drop collision, uninsured motorist property damage becomes your only first-party coverage for hit-and-run accidents. The annual cost is lower than collision, and the deductible is typically smaller.

Chandler's metro density and snowbird seasonal population increase hit-and-run frequency compared to rural Arizona. If you drop collision, confirm whether your carrier offers uninsured motorist property damage and what the deductible is. Some retirees keep comprehensive and drop only collision, preserving theft and hail coverage while shedding the highest-cost component. That is a valid middle position if your vehicle value justifies comprehensive alone.

Carriers Writing Personal Auto in Arizona

25

Twenty-five carriers write personal auto coverage in Arizona, including standard, preferred, and non-standard tiers. When comparing liability-only quotes, retirees with clean records often qualify for lower rates at preferred carriers than they paid under full coverage at their current standard-tier carrier.

NAIC state filings and carrier licensing databases

When Keeping Full Coverage Makes Sense

If your vehicle is worth more than five times the annual cost of collision and comprehensive, the coverage typically earns its cost over a reasonable holding period. A 2020 sedan worth $18,000 with $550 annual collision and comprehensive cost justifies keeping the coverage if you plan to drive it another four years. The ratio is the decision point, not the vehicle's age or paid-off status.

Retirees who drive fewer than 5,000 miles per year face lower collision risk than commuters, but collision premiums do not automatically reflect mileage reduction. If your carrier offers a low-mileage discount and you have not enrolled, request it before comparing quotes. Some Arizona carriers reduce premiums when annual mileage drops below 7,500 miles, and the reduction sometimes makes full coverage viable for another year or two on a moderately valued vehicle.

How Liability Limits Interact With Retirement Assets

Dropping collision and comprehensive does not change your liability coverage, but the decision often prompts retirees to review whether their liability limits protect retirement assets. Arizona's minimum is $25,000 per person and $50,000 per accident for bodily injury. If you cause a serious accident and the injured driver's medical bills exceed $25,000, they can pursue your personal assets to cover the difference. Home equity, retirement accounts, and savings are exposed in a judgment.

Many Chandler retirees carry $100,000 per person and $300,000 per accident liability limits, which cost meaningfully more than the state minimum but far less than collision on an older vehicle. When you request a liability-only quote, confirm your liability limits. If your current policy carries the state minimum and you own a paid-off home or substantial retirement accounts, increasing liability limits is often the better use of the premium you save by dropping collision.

Compare Liability-Only Quotes Now

Request a liability-only quote from your current carrier showing the same liability limits you carry today with collision and comprehensive removed. Compare that annual premium against your vehicle's current private-party value minus your deductible. If the cost of collision and comprehensive exceeds one-third of your net payout ceiling, dropping them returns premium dollars you can apply elsewhere or simply stop spending. Retirees in Chandler with clean records often find that switching to a preferred carrier for liability-only coverage saves more than the collision premium alone, particularly if the current carrier never applied a mature-driver or low-mileage discount.