Updated July 2026

What Is Collision Coverage Insurance?

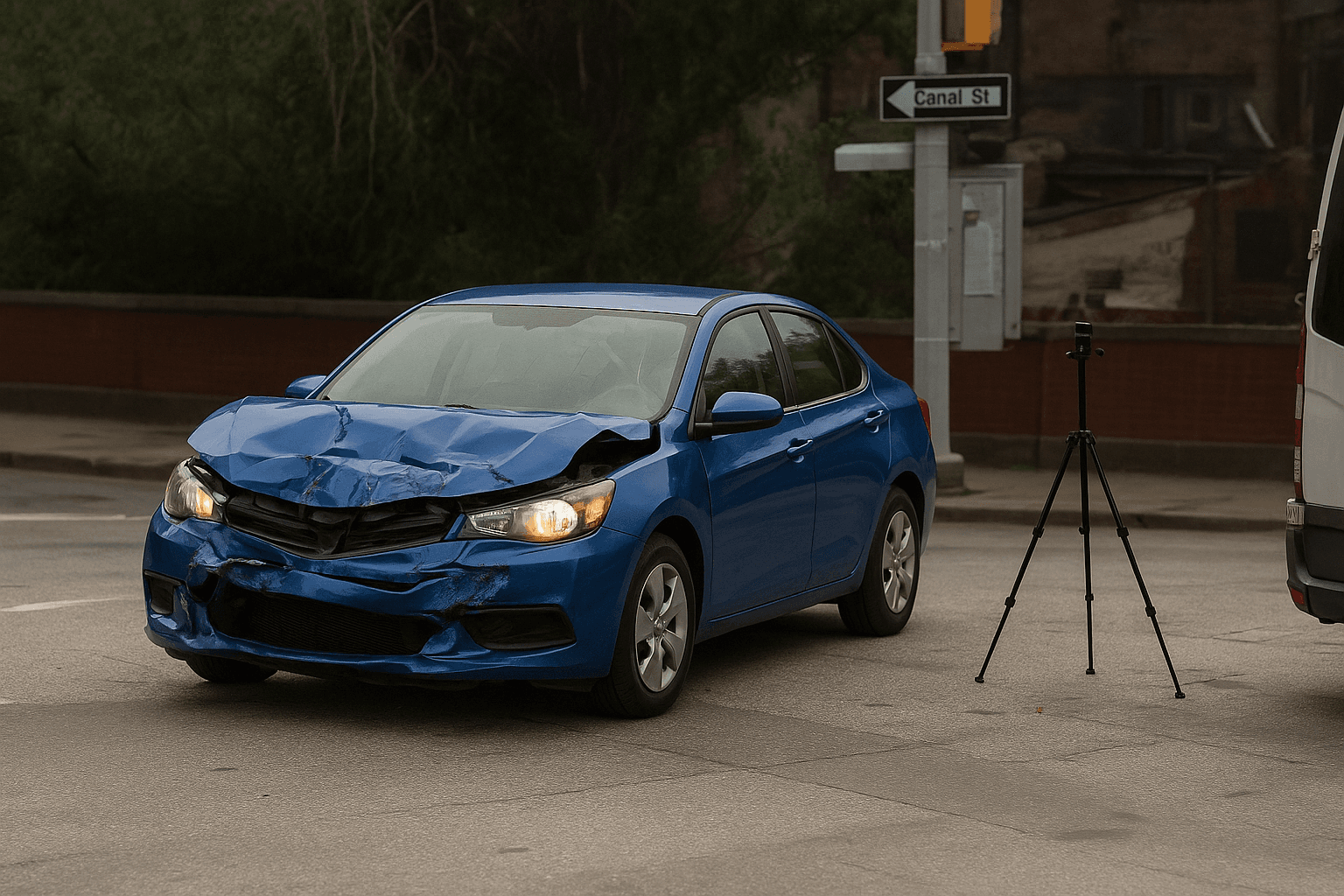

Collision coverage is an optional auto insurance policy component that pays for physical damage to your vehicle after a crash with another car, a stationary object like a guardrail or tree, or a single-vehicle rollover. It applies whether you caused the accident or share fault under Arizona's comparative negligence system. The insurer pays the repair cost up to your vehicle's actual cash value minus your chosen deductible, which typically ranges from $500 to $2,000. Unlike liability insurance, which Arizona requires and which pays the other driver's bills when you're at fault, collision coverage protects your own asset.

- You brake late and rear-end the car ahead at a red light. The other driver's vehicle has $4,200 in bumper and frame damage, covered by your liability insurance. Your own car needs $3,800 in front-end repairs. Collision coverage pays the $3,800 minus your $1,000 deductible, leaving you with a $2,800 check. Without collision, you pay the full $3,800 out of pocket even though liability handled the other driver's claim.

- You swerve to avoid debris on I-10 near Phoenix, lose control, and roll into a ditch. No other vehicle involved. Your 2015 SUV sustains $11,000 in damage, but its actual cash value is $9,500. Collision coverage pays the $9,500 cap minus your $500 deductible, netting you $9,000. The remaining $2,000 in repair costs exceeds the vehicle's worth, so the insurer totals the car and you receive the $9,000 settlement.

- Another driver backs into your parked car in a Tucson grocery lot and leaves no note. The damage is $2,400. If you have their plate and can file a liability claim against them, their insurance covers it. If not, your collision coverage pays the $2,400 minus your deductible. Many retirees discover here that a $1,000 deductible means a $1,400 payout for a $2,400 repair — often less than the premium paid that year to carry the coverage.

Who Needs Collision Coverage Insurance?

Retirees who financed a newer vehicle or leased a car must carry collision coverage until the lender releases the lien — the contract requires it. If you own a vehicle worth $8,000 or more and lack the cash reserves to replace it after a crash, collision coverage transfers that financial risk to the insurer for a predictable annual cost. Drivers with a history of at-fault accidents or who navigate high-traffic urban corridors daily may find the premium justified even on moderately valued vehicles.

Calculate your vehicle's actual cash value using Kelley Blue Book or a recent dealer appraisal, then compare that figure to your annual collision premium plus deductible. If the premium plus deductible equals or exceeds 30 percent of the vehicle's value, you're spending more to insure the asset than a likely claim would return. Retirees with emergency savings covering the vehicle's replacement cost can redirect the premium savings into those reserves and drop collision coverage.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $25 to $65 per month, or $300 to $780 annually, depending on vehicle value, deductible choice, and driving record.

- Vehicle age and actual cash value — older paid-off cars generate lower premiums because the payout ceiling drops as the car depreciates.

- Chosen deductible — selecting a $1,000 deductible instead of $500 can cut the premium by 20 to 30 percent.

- Annual mileage — retirees driving under 7,500 miles per year qualify for low-mileage discounts with most Arizona carriers, reducing collision premiums further.

- Driving record — a clean record over the past three to five years lowers collision rates, while at-fault accidents increase them for three to five years after the incident.

- Zip code — urban areas like Phoenix and Tucson carry higher collision premiums due to greater accident frequency than rural counties.

- Bundling with comprehensive coverage — carriers often discount collision premiums when you carry both collision and comprehensive on the same policy.